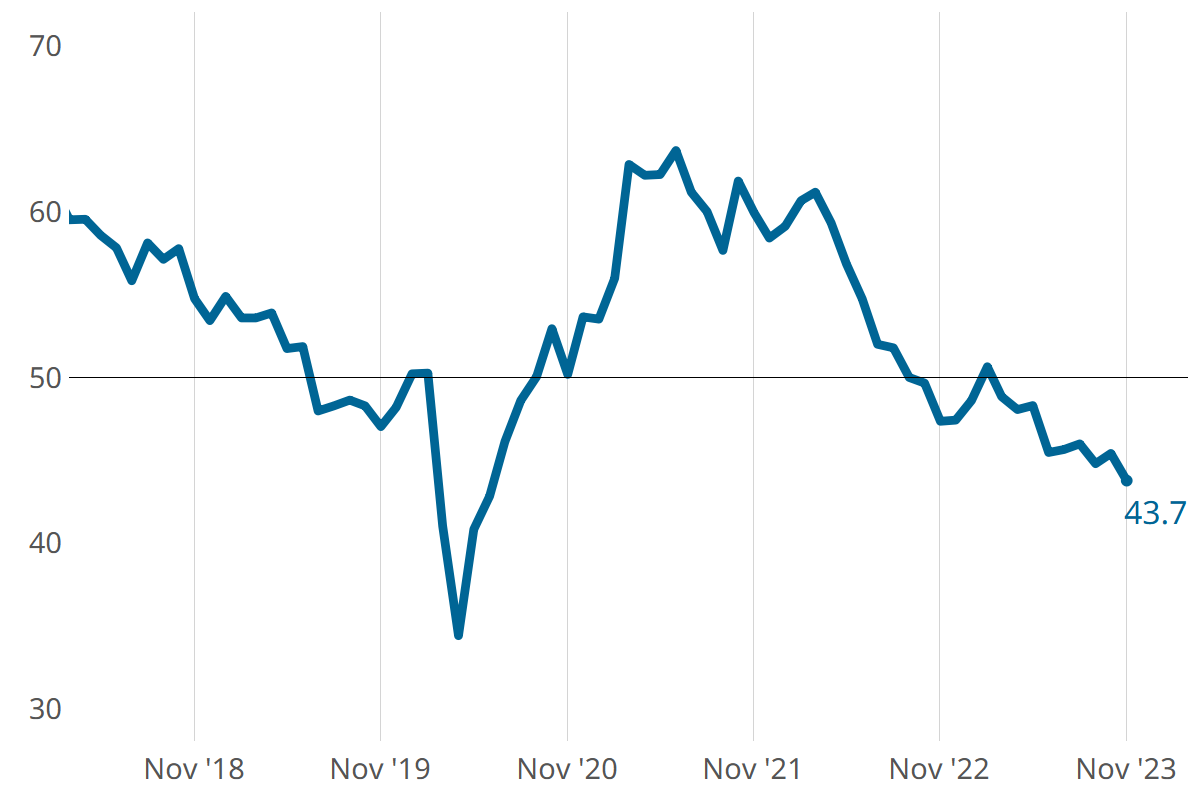

Metalworking Activity Remained on a Path of Contraction

Steady contraction of production, new orders and backlog drove accelerated contraction in November.

Share

The path has not been direct, but the trend is consistent, with metalworking activity contracting since March of this year. November was no different, closing at 43.7, down 1.7 points relative to October.

Steady contraction of three closely connected components — production, new orders and backlog — drove accelerated contraction. Employment held its own, contracting at the same level since its first real contraction in August, still to a lesser degree than all the other components. Exports were similarly steady state in contracting, and supplier deliveries lengthened again in November, but at a slower rate.

Metalworking GBI zigzagged down again in November. Photo Credit: Gardner Intelligence

The three most direct drivers of metalworking activity posted accelerated contraction in November, which they have done fairly consistently since March of this year (3-MMA = three-month moving averages). Photo Credit: Gardner Intelligence

Related Content

-

Metalworking Activity Trends Down Again in June

The Metalworking Index closed at 44.3 in June, down 1.2 points relative to May, marking a 2024 low.

-

Metalworking Activity Contracted Marginally in April

The GBI Metalworking Index in April looked a lot like March, contracting at a marginally greater degree.

-

Metalworking Activity Continued to Contract Steadily in August

The degrees of accelerated contraction are relatively minor, contributing to a mostly stable index despite the number of components contracting.