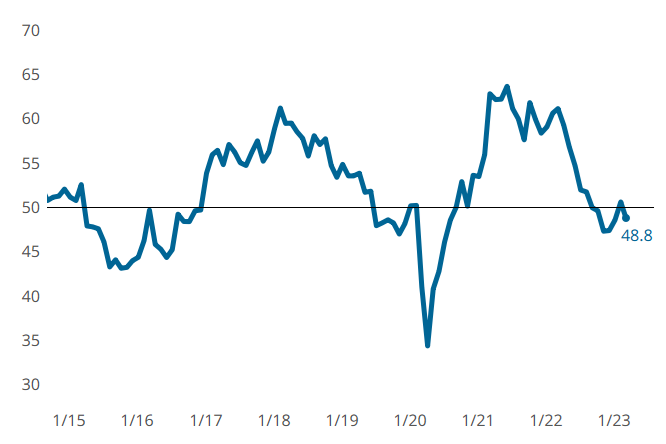

Metalworking GBI Contracted in March After One-Month Reprieve

February’s call for cautious optimism was well placed…market dynamics in March put a damper on what had been metalworking activity’s modest re-entry to growth mode in February.

Mikron Machining is the leading partner for high performance machining systems to manufacture complex and precise metal components in high volumes....READ MORE

HEIDENHAIN is a world-leading provider of encoders, machine controls, touch probes, digital readouts and metrology solutions—empowering engineer...READ MORE

Since 1965 we have been manufacturing precision metal products in the United States. We are a veteran-founded, woman-led business dedicated to mak...READ MORE

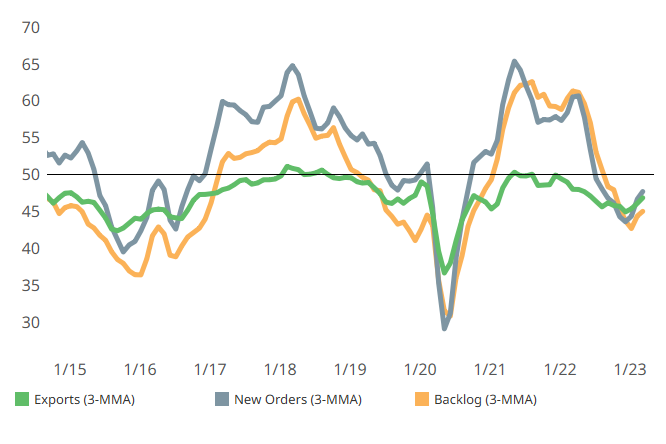

Five of six components continued to move in directions of contracting slower or growing faster (employment) on a three-month moving average.

The same types of movement in the same components were associated with a GBI that had tiptoed out of the (contraction) woods last month. Caution appears to have crept back in March.

Additional evidence of caution comes from the future business metric (separate from GBI calculation.) It had been expanding, reflecting growing optimism each month since December 2022, but leveled off in March.

Production slid into growth mode (just barely…) in March for the first time since August 2022.

New orders, exports, and backlog still contracted in March, again at a slower pace.

Supplier deliveries continued to lengthen more slowly as supply chain woes wane.

It appears that while optimism was tempered in March, pessimism was kept at bay to net a month of solid metalworking activity.

Metalworking GBI contracted again in March after a one-month reprieve.

More of the same (slowing contraction) for components, new orders, exports, and backlog is associated with metalworking’s modest GBI downturn in March.

The GBI Metalworking Index in April looked a lot like March, contracting at a marginally greater degree.

Advertisement

Advertisement

Advertisement

Advertisement

Advertisement

Advertisement

Advertisement

Advertisement

Advertisement

Loading

Next Up

Why am I seeing this?

The page you’re on features premium MMS editorial content.

To continue enjoying the articles, videos and podcasts from the MMS editorial team, please key in your name and email address, as well as your company and title info.

Doing so unlocks MMS’ premium web content on this device.

Why does the gate appear repeatedly for me?

If the gate continues to show up on premium content after you’ve already provided your information, it could be for one of these reasons:

Your cookie settings: Please allow cookies for www.mmsonline.com

You’re browsing in incognito mode. Switching out of private browsing mode may help.

You are viewing on a different device or browser. Your login is connected to the browser and device on which you originally unlocked MMS’ premium web content.

More of the same (slowing contraction) for components, new orders, exports, and backlog is associated with metalworking’s modest GBI downturn in March.

More of the same (slowing contraction) for components, new orders, exports, and backlog is associated with metalworking’s modest GBI downturn in March.